Blockchain and banking: Key benefits and challenges

This pioneering technology is essential to most cryptocurrencies, but blockchain could revolutionize banking too.

When you hear or read about blockchain technology, chances are it calls to mind Bitcoin and other forms of cryptocurrency. That’s because blockchain is the underlying technology that allows for the exchange of most digital currencies. Yet blockchain proponents point out that it has other current and potential applications across many industries, such as improving supply chain management and the tracking of health care and real estate records, for example.

What’s more, 90% of U.S. and European financial institutions are exploring blockchain, according to the Blockchain Council, a collective of experts dedicated to promoting the technology. “The trajectory of blockchain technology in banking is increasing slowly but steadily,” says Greg Miles, head of treasury management products and services at Regions Bank.

What is blockchain?

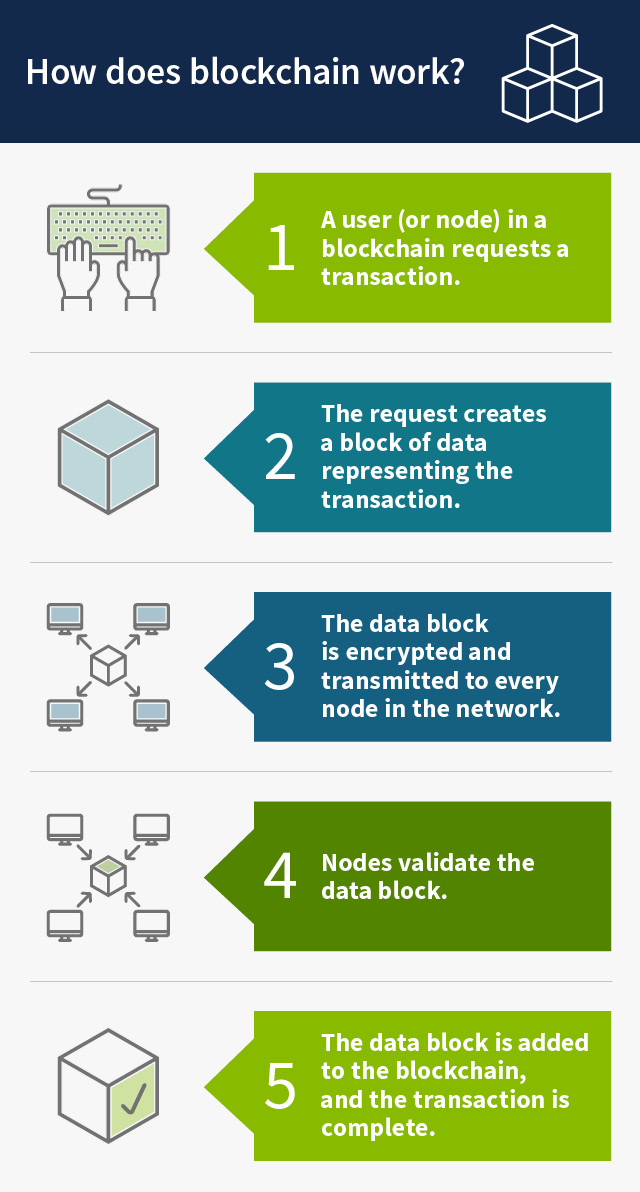

Blockchain consists of a chain (or collection) of blocks (or chunks) of transaction data. It uses distributed ledger technology, which means the entire blockchain is continuously shared across a network of computers instead of the traditional centralized approach of a handful of parties—at most—maintaining records. Data entered into a blockchain is permanent and irreversible.

“What distinguishes blockchain from a lot of other technologies is that this multitude of computers are all acting in concert,” says Miles. “The fact that the records are created simultaneously and on multiple computers gives these transactions unique transparency and security because it would be hard to deceive the many other computers that are recording the same transaction at the same time.”

This feature of blockchain alone should appeal to anyone concerned about ransomware attacks by bad actors who hold data hostage for a high price. “It is significantly more difficult and almost impossible to imagine holding data hostage when it’s in a decentralized environment,” says Miles.

How might blockchain transform banking?

“Blockchain is uniquely suited to banking,” says Miles. Blockchain allows Bitcoin, Ethereum and most other digital currencies to be transferred from one party to another without the need for several extra middlemen. The lack of added intermediaries in blockchain, as well as its security and other features, could make the digital exchange of monetary information more efficient—and even potentially safer.

Miles says the following financial transactions could benefit from the technology:

- Smart contracts. By automating and enforcing contract terms without the need for these extra intermediaries, blockchain-based smart contracts can, in some cases, enable faster and more transparent execution of financial agreements. Smart contracts can automate required events based on contract terms, such as the disbursement of funds based on the receipt of goods in a warehouse, or the release of freight from a port once customs has approved the contents. “You can’t talk about blockchain for long without talking about smart contracts,” says Miles.

- Account-to-account payments. That could include business-to-business, business-to-customer or person-to-person payments. When these transfers are entered on a blockchain, they’re rapidly recorded with both parties’ banks, which dramatically reduces processing time.

- Cross-border payments. These transactions often involve multiple banks or other financial institutions and require verification by numerous intermediaries, slowing the process. By eliminating intermediaries, blockchain reduces settlement times, expediting these transfers, and trimming costs for companies and individuals alike.

- Securities holdings. Distributed ledger technology creates an accessible record of stock and bond ownership with the added benefits of heightened security and transparency. These qualities will be especially attractive to buyers and sellers of sophisticated securities holdings such as syndicated loans and derivatives.

- Trade finance. By providing a transparent and tamper-proof record of transactions, reducing paperwork and improving efficiency, blockchain could streamline trade finance processes.

- Asset tokenization. Blockchain can tokenize assets such as real estate and securities, facilitating fractional ownership as needed, as well as liquidity and access to a broader investor base.

Other benefits of blockchain

Blockchain can provide a secure, decentralized way to verify customer identities, which could reduce the risk of identity theft and improve customer onboarding processes. “I think this is potentially a very large area of opportunity for blockchain,” says Miles.

Blockchain could also enhance Know Your Customer (KYC) and anti-money laundering (AML) procedures by securely storing and sharing customer information among banks, improving regulatory compliance and reducing fraud.

Another less discussed potential upside to the wider adoption of blockchain technology is increased inclusivity. By reducing the involvement of multiple intermediaries, blockchain could create easier access to financial services for underserved populations by providing secure and efficient ways to conduct financial transactions, says Miles.

Challenges to implementing blockchain-based solutions

While blockchain could revolutionize the conduct of financial transactions and other business, that will require overcoming some potential obstacles.

- Interoperability. Most blockchains operate in isolation with unique rules and data structures. A lack of interoperability could hinder seamless data exchange between blockchains.

- Regulatory issues. Miles believes rules established by the U.S. Securities and Exchange Commission and other regulatory agencies will ultimately have the greatest impact on how and whether blockchain changes the way banks and other institutions conduct business. “However, the very nature of blockchain could actually help ensure compliance with regulatory requirements by providing a transparent and auditable record of monetary transactions,” says Miles.

- High energy use. Much attention has been focused on the massive amount of electricity required by data centers that house computers in blockchain-based cryptocurrency networks. The annual electricity use from cryptocurrency mining accounts for between 0.6% and 2.3% of electricity consumption in the United States, according to the U.S. Energy Information Administration. “This demand for electricity has drawn the attention of policymakers, environmental advocates and grid planners about its effects on cost, reliability and emissions,” says Miles.

- Scalability cost. “Scaling blockchain networks to handle a high volume of transactions quickly and efficiently is going to be a challenge, especially for public blockchains,” says Miles.

Miles is optimistic that these potential hurdles won’t prevent blockchain from emerging as a powerful force in banking. Regions doesn’t currently participate in any blockchain networks, but the bank is studying the technology. “We have proven we can use blockchain,” says Miles. “We want to ensure we are able to adopt blockchain technology when the time is right—when it meets the identified needs of our clients.”

Three things to do next

- Read more: 3 key steps in developing a digital transformation strategy.

- Learn more: Watch our video intro to cryptocurrencies.

- Take action: Safeguard your organization as you shift to digital.

Related Insights

-

Article

Article

-

Calculator

Calculator